Our goal is to change the internet architecture to one that is software-defined and fully programmable.

The Internet for enterprises today completely sucks. Service offerings are simply insufficient and they only slow enterprise growth potential and critical digital transformation.

Enterprises are forced to choose between bad and worse: antiquated hard-coded, inflexible network services or consumer quality connectivity wrapped in a higher price tag, with symmetric up/down speeds and delivered into a swamp of intermixed consumer and business traffic. The offers are mostly disparate service capabilities built out of a patchwork quilt of technologies that have become too complex to own and operate at a time when staff can’t be found to do the basics.

What can be acquired and built over-the-top of public networks today is inflexible and static in the most rudimentary of network topologies: hub and spoke like a wagon wheel or a web of VPNs. The assumption of ubiquitous reach is a fallacy and the notion of infinite internet bandwidth availability to sustain every need, is just plain wrong. The internet for enterprise is anything but ubiquitous and infinite; its reach is limited and bandwidth is constrained.

As a remedy, an enterprise can hire a solution integrator to build a bespoke nightmare draining them of their emotional stamina and their wallets. Or, they can choose to be hobbled by a CSP or big DCO with a dependence on a single island of connectivity which limits reach and flexibility. Any notion of hybrid or multi-cloud is immediately thwarted or made overly complex, and any desire to use a suite of SaaS security, storage or UC clouds is further dampened by closed ecosystems.

Businesses cannot remain hobbled by legacy telco’s reach which offers no cloud connectivity and lacks meaningful control of bandwidth or latency. Telco services are far behind what’s required by Enterprises today. Any notion of telco modernization are mere thought-exercises, improvements as part of their 2030-decade planning.

The heralded and overhyped technologies of the last 15 years are mere bandaids to overcome the limitations of MPLS-VPNs and other telco cement: express paths, direct-connects, even SD-WAN and their internet overlay ilk all need to be scraped from enterprise network engineers’ way of thinking.

As an industry we need to end the complete fallacy that an enterprise’s secret sauce is how to operate and manage their network and that they have to own it to trust it.

To be perfectly clear, “Enterprise Digital Transformation 2.0” (because we used the same tagline 20 years ago) is going to be completely hamstrung without a fundamental change in enterprise’s ability to control connectivity, bandwidth, latency and cost to break the chains of bondage of telcos, CSPs and DCOs.

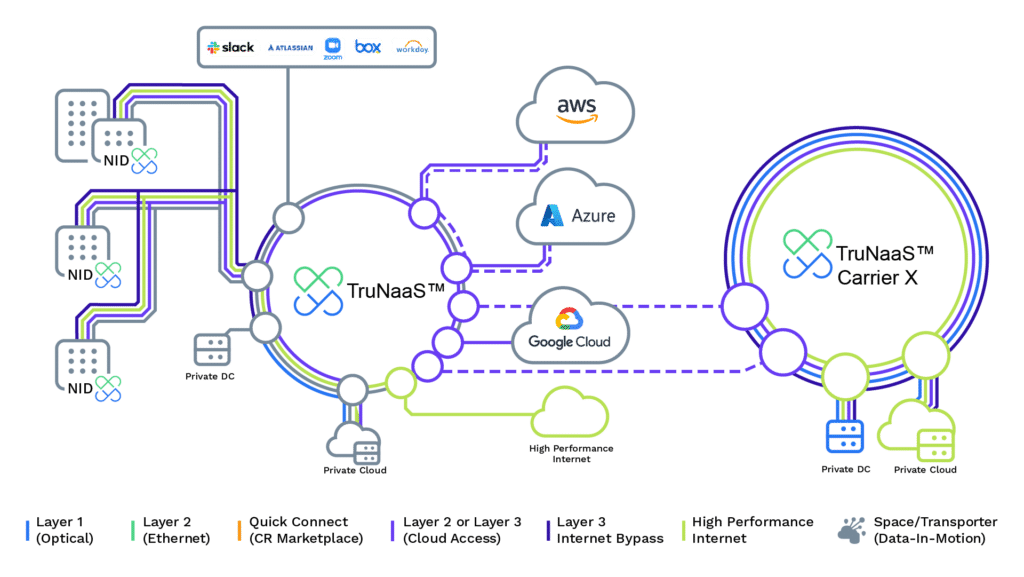

What is needed is a re-imagination of business operations enabled by a fully programmatic Internet infrastructure: connectivity on demand, full bandwidth and latency control, from the building/campus to all clouds (CSPs, DCOs, SaaS, security, storage, UC) and the internet.

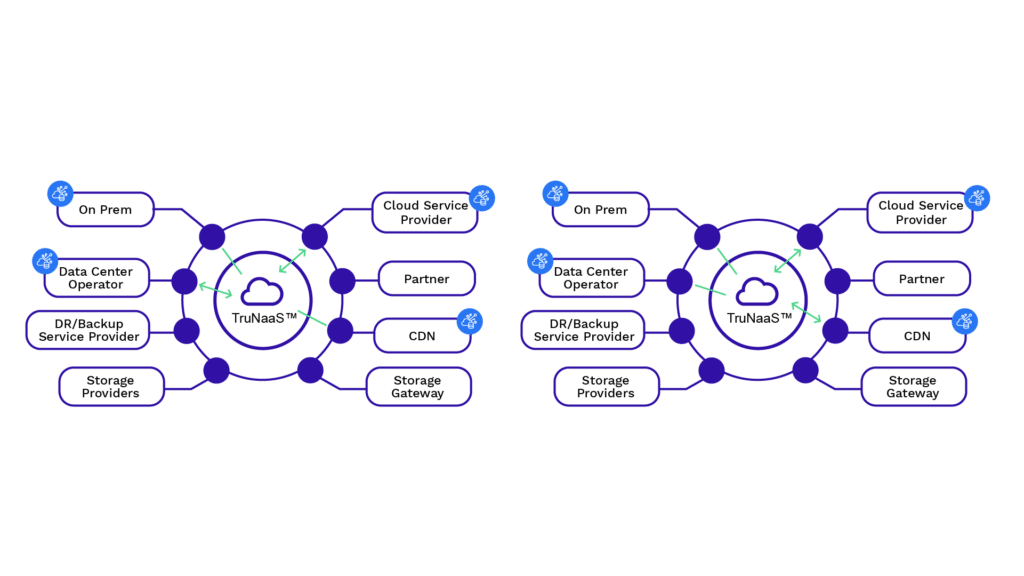

This is the exact target of PacketFabric: We are a 100% self-controlled, real-time, on-demand; secure, private Internet for enterprises.

We have bandwidth and latency controls, full redundancy, guaranteed SLAs, a pay-for-what-you-use, optimal fabric topology for forwarding/routing, all operated and managed like a SaaS. We deliver true NaaS (Network as a Service) in an unprecedented way: Edge to Everywhere, from in-building/campus to all the clouds, all the services and the internet.

PacketFabric has built a SaaS offering for fully programmatic secure, private Internet services. It can be driven by a UX or by APIs depending how tech savvy the enterprise is, and can be integrated into workflow management (devops), data-in-motion demands or network operations tooling (netops)..

PacketFabric is a visionary network operator with the assets of a software company purpose built to revolutionize telecommunications.

I. It’s a platform and all about being a platform

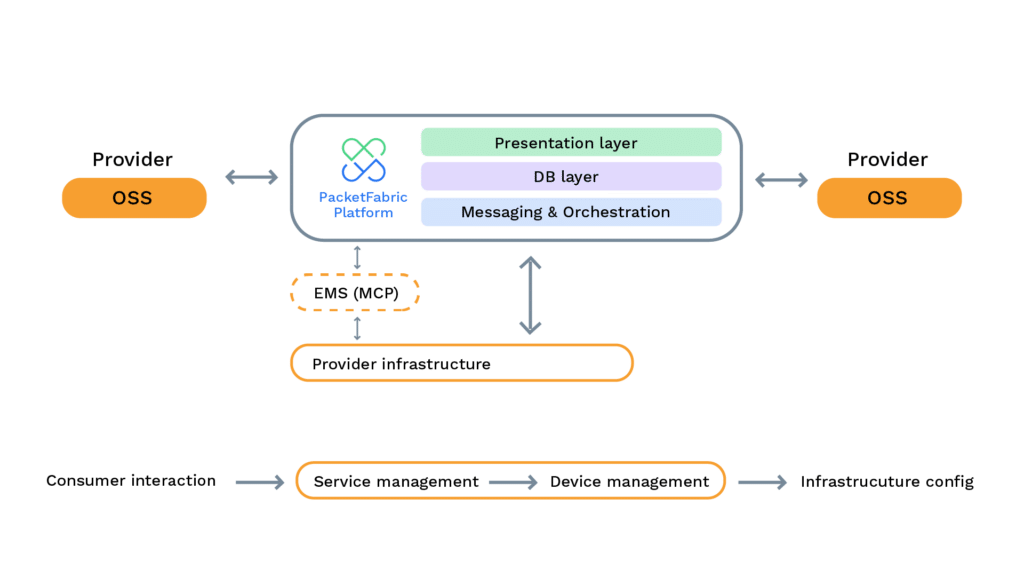

The PacketFabric Converge platform addresses three main Network Automation use cases: Network Orchestration, Service Orchestration and Deployment. We have an embedded accounting and billing capability, provide full monitoring ability, and with our API-first structure, our core architecture can be integrated with an existing partner’s BSS, OSS or domain specific EMS.

This capability is critical as we make the turn toward providing platform services, because our potential partner providers and software consumers have historically been addicted to multi-billion dollar legacy OSS/BSS systems with tentacles spanning multiple product divisions.

We understand that it’s an extremely hard addiction to break. While we can stand alone as a separate platform for a discrete set of products, we know it is also important to be able to coexist in the context of these legacy systems.

Unlike the incumbents in the Network Automation space, PacketFabric positions as a potential PaaS and not as hierarchical controllers (existing vendors solution architectures), and our integrated BSS drives a potentially larger value proposition than competitive products based on legacy constructs.

What We Do

We bring a fundamental technology and business disruption to Connectivity Services:

- A cloud native, scale-out SaaS platform on top of our connectivity services provides frictionless, on-demand, self-service from the building/campus to all clouds and the internet.

- We have added a second, cloud native access line platform and wholesale marketplace in 170+ countries around the world, specializing in designing, pricing, and ordering end-to-end connectivity.

- We offer a cloud style model for connectivity services, providing an independent, neutral, vertically-integrated and scalable true NaaS platform,

- We have developed a frictionless model for partnering with telcos and DCOs to efficiently scale revenue and expand margins.

- We have aligned a coherent strategy to disrupt the legacy communications industry with fundamentally different models of pay-for-what-you-use, burstable and terms from hourly to three years between endpoints, and aggregate capacity which applies a total-bandwidth model to a changeable set of endpoints across our fabric.

Our target is the mid-market and larger enterprises and their solution providers, with needs for private business-only networks, willing to pay a premium for reliability, SLAs, bandwidth and latency control and the agility of a cloud consumption model.

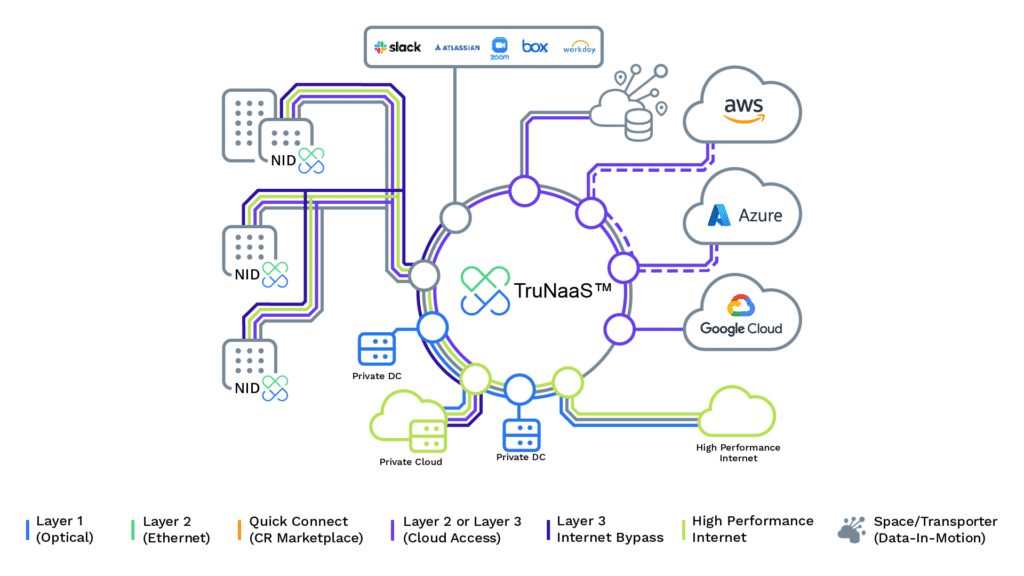

The addition of leading business internet services, private peering and transit from our merger with Unitas Global creates compelling IP connectivity for our NaaS clients that need to interface public network access with the private, secure connectivity of a true NaaS.

The PacketFabric business model builds end to end connectivity solutions, from in-building WAN underlay control to the access line to the core. It’s the creation of underlay services (meaning not riding on the consumer internet) and connectivity options.

PacketFabric, with the combined automation of PacketFabric and Unitas Global, envisions a Network as a Service opportunity that goes beyond cloud on-ramps and middle mile – but to EVERY mile; first, cloud and Internet.

We are a true NaaS platform built around the basic NaaS principles of automation, self-service and consumption model economics with the additional exclusive and fundamental constructs of a true NaaS: purpose-built and market neutral with easy service integration and extensible to over 50 million buildings.

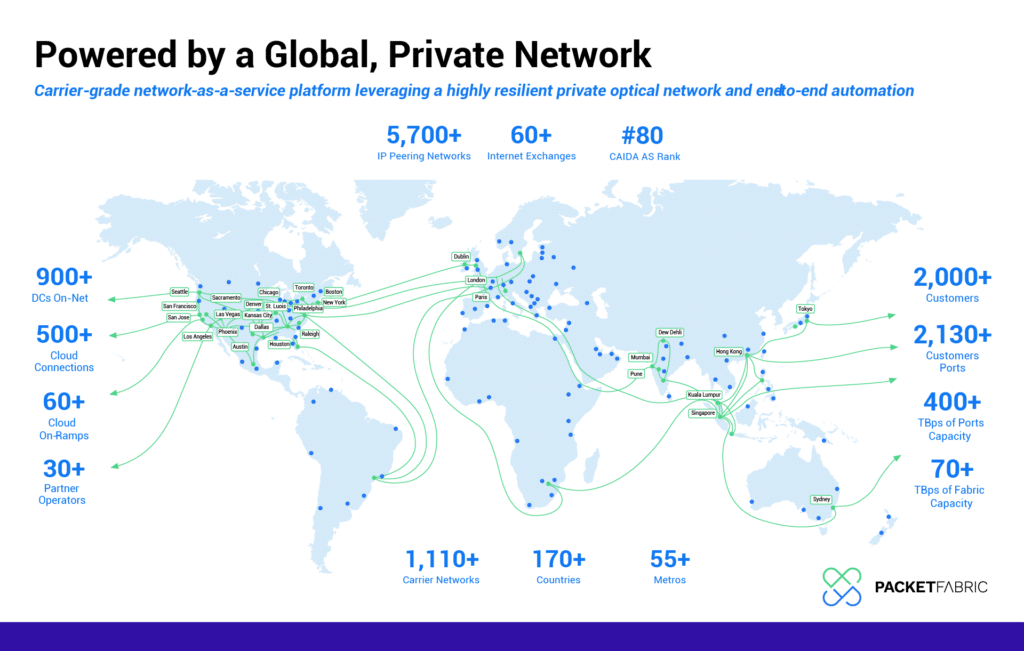

At our size and scale, we are co-oper-competing with Telcos but with a very specific focus: business services. The locations in blue below reflect locations where we are currently deployed, the green represents areas of expansion. Our network reach enables us to serve both regional and multinational businesses.

- In our NaaS fabric core, we continue to integrate the latest advanced technologies – including 400Gbps ports, multi-path multi-100 Gbps interfaces, a multi-provider ecosystem with all major hyperscalers (over 62 public cloud on ramps), SaaS providers and 30 DCO partners in 57 metros with a capacity over 69 Tbps.

- Our transit services appear at 59 global exchanges and peer with over 5600 IP networks, with optimized MIRO exit routing.

- Our core fabric reach now extends to over 175+ additional connectivity PoPs, accessing 1,000+ providers, 50M+ edge locations, 900+ DCs, and 6,000+ SaaS providers, in 180 countries.

- We go further than any other NaaS or service provider in using distributed systems to scale our platform’s performance. We offer both ReST API and streaming telemetry for monitoring of services with AI-based proactive notifications. We give our customers full operational visibility into their network and our performance; again, in real-time.

- PacketFabric provides a fully programmable private network, business Internet, and cloud access.

Why automation, self-service and consumption model matter

From both a provider and customer perspective, automation and self-service replace legacy netops and bizops. Consumption model economics replace legacy telco billing and rigid long-term contracts.

We apply this model across the entire range of Enterprise connectivity needs, resulting in tangible business benefits to our customers and partners:

- Business Facilitation: For our customers, even in the cases where physical work is required to provide service, we apply our “automate everything” motto to the surrounding processes – eliminating paperwork delays, phone calls and ambiguity to provide a streamlined experience and making it incredibly easy to work with PacketFabric.

- Easy Integrations: The automation visible in our cloud-first orientation and API-driven focus make our platform and solutions easy-to-integrate. Our complete API coverage and support of Terraform enable the most sophisticated users of the business network as well as our network service and telco partners to integrate our NaaS services into their automation and management software.

- Immediate fulfillment: For our customers and our partners, our self-service portal puts the creation or modification of services directly in your hands, providing the best customer experience at the lowest cost. For those customers not ready for self-service, our sales staff and resellers can help and you still benefit from the immediacy of fulfillment that a NaaS operation implies – on-demand, real-time services. The resulting benefits are a superior quality of service and customer satisfaction (reflected in high provider CSAT and NPS scores).

- Cost Flexibility and Predictability: Consumption model economics of NaaS decreases customer costs by enabling pay-for-what-you-use elastic capacity, a key tenet of LeanIT for CTOs and CIOs alike. Capacity when you need it, eliminating stranded capacity problems that have accompanied the traditional WAN operational models NaaS replaces. Flexible bandwidth “use it where you want”, and predictable fixed-rate, usage-based consumption (from sub-1Gbps to multi -100Gbps) in our fabric. Up to 50-70% cost savings on cloud egress charges. Greater visibility into available options (with pricing) for access.

Taking Automation further – into Access

PacketFabric is currently taking automation even further into a fundamental disruption of the most opaque areas of enterprise networking – first/last mile access – via Nexus.

Nexus is a proprietary software platform designed like our core NaaS as a neutral ecosystem marketplace. It provides price and route transparency over hundreds of participating providers with the ability for the customer to orchestrate solutions, through Nexus policy mechanisms, over multiple networks and provide visibility into performance and health.

Nexus provides the automation to design, price and order end-to-end services including first/last mile to their premise in 170+ countries across more than 1100 access networks.

Designed to be the “Expedia for edge,”, Nexus removes the complexity of first/last mile circuits for over 50 million fiber-lit buildings. Those buildings have different fiber fed services, but across the differing providers; we can create a unified enterprise network. Nexus demystifies the stacking and variability of services to make creating fiber between buildings easy.

While the Nexus wholesale marketplace can be used by anyone (as a separate stand-alone service), Nexus will enable fungible multiservice network design when combined with a programmable deployment controlled by the PacketFabric Converge platform. This will allow customers to change/reallocate capacity and function on demand, enabling flexible consumption and utilization of the network.

Nexus and the PacketFabric will potentially extend our true NaaS to over 50 million fiber lit buildings and enable multi-provider facility to PacketFabric connections, stitched together through partner NNI/API on our fabric at our PoPs. We’re connecting business endpoints with capacity to DCOs, CSPs, SaaS and the public Internet requires different connectivity from a tactical perspective – DIA, (E)VPL and more – and are inherently multi-service.

Our vision is to enable the PacketFabric API to deploy and orchestrate the Edge/NID services instead of using externals like Service Now (human capital driven) and add capability like SDWAN via partners by teaching the Nexus orchestration API to talk to other orchestration APIs for design and deployment of a network.

While last mile services ‘time to first deployment’ remains the long pole, NaaS innovates back office processes to make even these operations an on-line experience – all trackable, no calls needed.

Best Platform and network in market to unlock a Data Fabric

In their recent 2022 NaaS provider survey, GigaOm stressed the importance of integrated storage as a future NaaS service, saying “Companies that use a lot of cloud storage and have to work frequently with this data should pay attention to integrated storage capacities…Cloud-integrated network storage (CINS) will become an important feature for two reasons: high egress costs for hyperscalers, which can quickly become a cost trap in agile infrastructures and hybrid and multi cloud scenarios and disaster recovery.”

Gartner’s Hype Cycle for Storage and Data Protection Technologies, 2022, emphasizes the expected growth of edge and hybrid cloud object storage over the next 3 years.

- By 2026, large enterprises will triple their unstructured data capacity stored as file or object storage on-premises, at the edge or in the public cloud, compared to 2022.

- By 2025, 60% of I&O leaders will implement at least one of the hybrid cloud architectures, from 15% in 2022.

- By 2025, more than 40% of enterprise storage will be deployed at the edge, up from 15% in 2022.

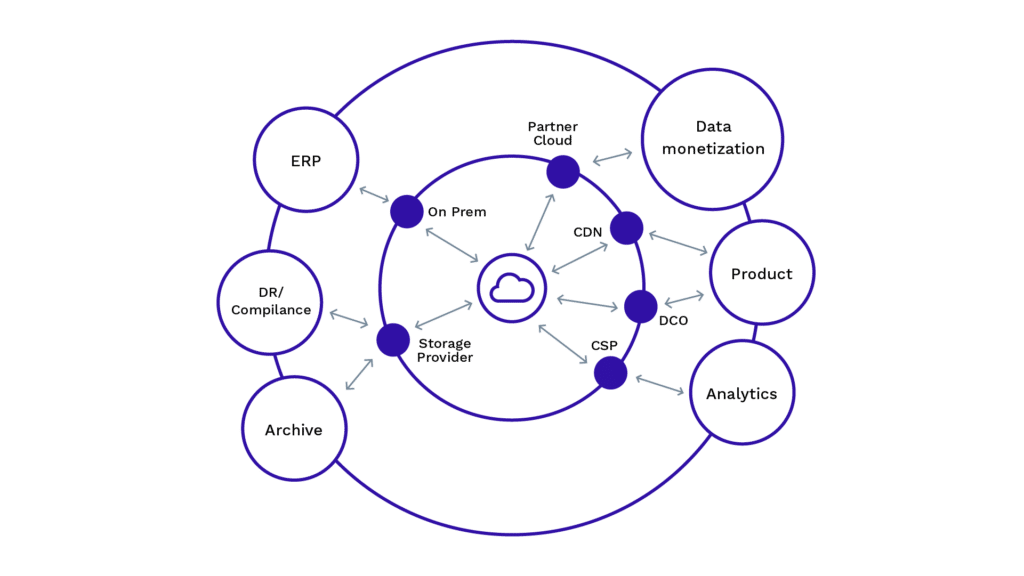

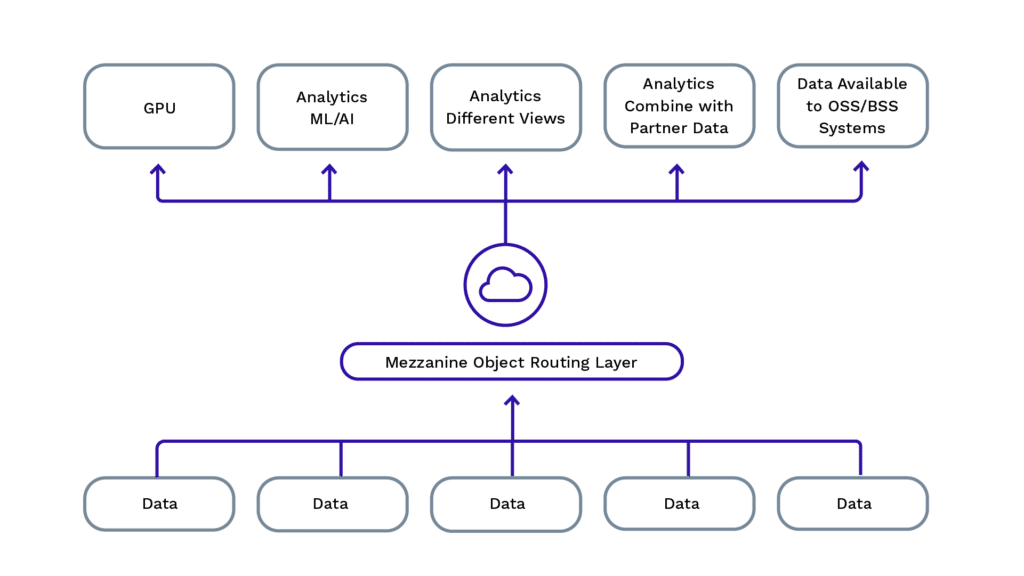

Enterprise workflows are moving toward a constant pipelining of objects across a broad, multi-cloud topology. Optimizing these workflows requires a high-speed programmable network and an intelligent object routing layer, or a mezzanine. The ability to move data at the speed of the business and optimize for a customer-defined set of business rules is the big prize at the end of the Golden Road, and this is what we’ve built.

PacketFabric’s Data-in-Motion service provides a mezzanine object routing layer – a pipe and object mapping service – that bends data “gravity” toward points of greatest need. Expanding and contracting bandwidth to support relationships between data storage endpoints; on-premise, CSPs, DCOs, DR/Backup Service providers, partners, CDNs and in-fabric storage partners.

Data should always gravitate to the points of highest access or computational value. A dynamic, programmable network is crucial to keep data moving through the mezzanine and toward higher-value targets.

Data-in-motion is a programmatic linkage between the physical storage ecosystem, storage orchestration, and the network. Dynamic speed, object placement, and bandwidth/connectivity changes allow objects to move around a topology following a programmatic set of criteria and business rules.

DIM links storage orchestration, analytics and physical storage for dynamic placement.

- STORAGE ANYWHERE is an in-network storage service for optimizing “data-in-motion” across multiple storage providers serving different purposes. We offer data movement and mezzanine services across any S3 service or endpoint, agnostic to storage cloud or provider.

- DATA-IN-MOTION TRANSPORTER is an application that enables (any) cloud-to-cloud data movement. High-performance S3 APIs, combined with PacketFabricGlobal connectivity APIs, provide dynamic placement of objects according to a customer’s specific business requirements.

- DATA MOVEMENT SERVICE CATALOG is a set of APIs that allow for easy-to-use abstractions such as “move data from point A to point B at X speed” as well as fine-grained control mechanisms that allow customers to set more sophisticated business rules to optimize for different pipelines and workflows.

Using our DIM services, customers can take advantage of storage as a network service to optimize for their most important business criteria. For example, if a customer wants to optimize for speed, they can dilate the network to move 30 PB in a month over a 100G link. If they want to optimize for cost, they can contract the network to meet a set of cost requirements. Objects can be tagged and differentiated dynamically to provide intelligent routing across multiple storage services.

The integration of data-in-motion as a fabric service (Mezzanine Object Routing Layer) has also led to the enhancement of our BSS to support object/volume motion billing and the resale of different storage clouds.

More Insight with Edge to Everywhere OAM/SLA

Although we are disrupting buying patterns with our service offering and network orchestration automation, we don’t sacrifice service visibility or reliability. In fact, we go further than any other NaaS or service provider with deployment of OAM and distributed systems to scale our platform’s performance. We give our customer’s full visibility into their network and our performance; again in real-time. Our goal is to enable AIOps, via APIs, by our customers in the same way we use the technology within our own platform.

We provide Edge-to-Everywhere monitoring and SLAs.

We offer both API query and streaming telemetry for monitoring of services: APIs can be used to present continuity management information from partner networks. Programmable thresholds, alarms, informs, customized alerts; ultimate customized visibility.

Our mantra is to automate and integrate everywhere we can: internal DevOps, SecOps, AIOps, NetDevOps, workflow management and other external service providers (e.g. SASE/SSE) . Using our APIs customers can break the barrier to agile private WAN consumption AND enable internal and external services required to support the digitized Enterprise. NaaS can provide the granular private connectivity missing from all other service adjacencies.

Deploying an on-prem edge device (aka Network Interface Device – NID) means we have 100% visibility into access providers networks. We can see everything: all drops, any fluctuations in service quality and run active and on-demand OAM. Additionally, in each of our network POPs we have an adjacent compute platform (in the distributed system) that runs full OAM as well as distributed data collection, measures latency, enables us to pre-provision images, configure and perform analysis on the devices, probe, and aggregate accounting data.

We’ve integrated the redundancy zone concept familiar in IaaS compute in our network design. As in the cloud where you choose to run your application in specific zones; we’ve mapped that concept into the network. A customer can choose to have their ports and services mapped to a zone where they know both that they have completely diverse routing/switching hardware redundancy as well as diverse fiber/spectrum to each zone. No longer is redundancy an issue; we’ve made everything we do multi-way redundant by default.

Where we sit in the industrial landscape

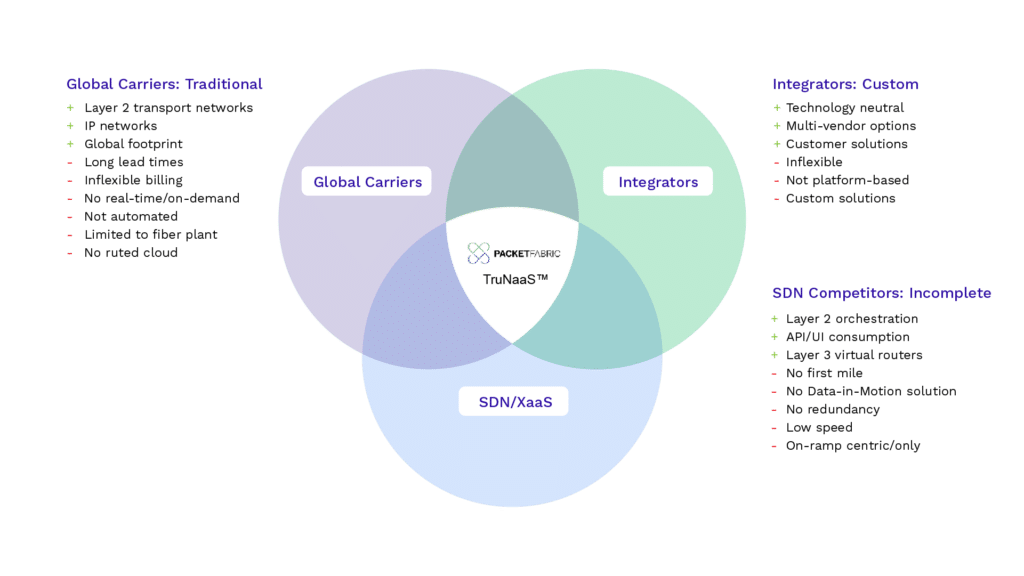

PacketFabric holds a unique position in the industry because we have built a complete multi-service platform focusing on all aspects of Enterprise connectivity, including storage and last mile.

- Our IP portfolio and automation significantly differentiates us from the rest of the market

- PacketFabric remains neutral in its approach, providing a private, highly scalable, highly secure service not limited in connectivity by CSP or DCO

NaaS is a complex arena, with many players claiming to play in the space, with varying degrees of success:

- We are winning share from competitors who focus primarily on a subset of the future connectivity services opportunity (eg. cloud onramps), lack the robustness of our long-haul fabric, have no access-line service or strategy and no data-motion offering.

- We’re taking share from the few DCOs that have attempted NaaS but self-limit their reach to their own properties.

- We are taking share from Global Carriers and large Integrators that lack comparable automation, self-service capabilities and consumption model support.

- GigaOm stated in their October (2022) Radar Report on NaaS, “With regard to the evaluation metrics…PacketFabric… achieved the highest score in all metrics…in contrast, vendors such as Megaport and NTT, with a continued strong focus on connectivity, remained in the Maturity quadrant.“

Because of their encumberments, some of our biggest competitors present an opportunity for PacketFabric to sell them on or both of our automated platform services.

II. What is the opportunity? All Tailwind

PacketFabric Opportunities: GTM

PacketFabric sees significant opportunity in both the Enterprise Communication Services market and disrupting the legacy telco OSS/BSS.

These opportunities will be realized through:

- Direct and Indirect Sales to Enterprise customers

- White-Label /Platform as a service (PaaS) offerings to telcos and DCOs lacking NaaS capabilities

What we are proposing is nothing less than demolishing the software boundaries that constrain traditional telecommunications.

NaaS Opportunity

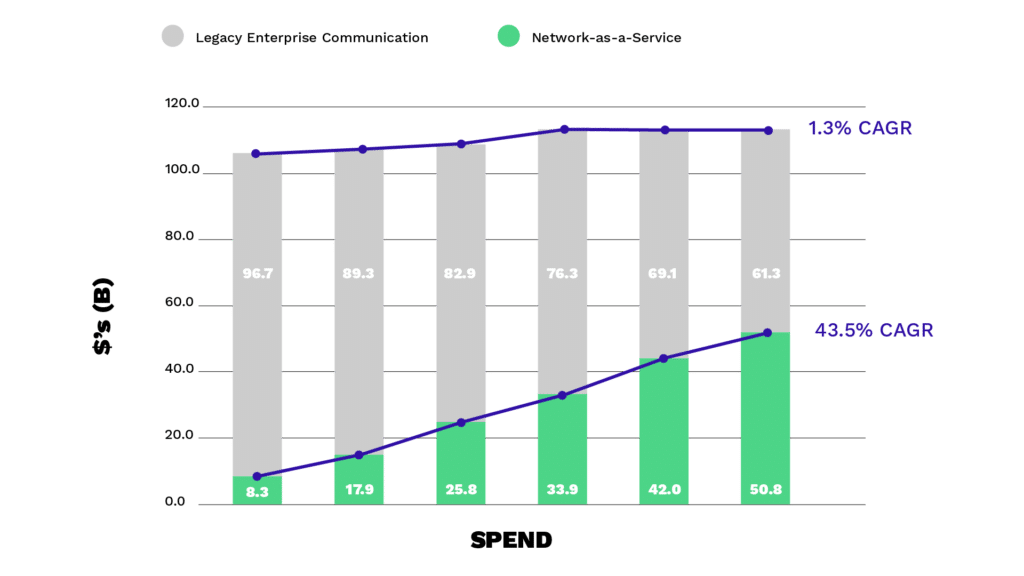

As an operator, we compete in a rapidly growing services segment with an estimated TAM of over $105-112BB by 2030.

We estimate the opportunity to address a subset of this TAM, with NAAS being $18B in 2027 growing at a 43.5% CAGR. Contrast that with the traditional Enterprises Communications Services Market which has historically suffered from anemic growth, and looking ahead, the prognosis is not better. Gartner estimates total aggregate Enterprise services communications revenue 1.3% CAGR over the next five years.

Why Is NaaS growing at such an attractive rate?

Analysts across the board note many different market drivers, converging and accelerating in a post-pandemic, altered workplace model, struggling to adapt to changing business needs, geo political turbulence and cost sensitivities. The drivers that stand out include:

- Adoption is poised to take off: by the end of 2024 15% of all enterprises will adopt NaaS, up from 1% in 2021.

- Spending on data center interconnect alone is expected to reach $18.3B by 2027, which represents a 13.9% CAGR from 2022 to 2027. And NaaS in Enterprise connectivity and telco operation is much more than just data center interconnect or cloud onramp.

- Adoption of cloud-based management for IT Services will grow from 15% in 2020 to 30% 2021 and cloud connect services will grow at double that pace.

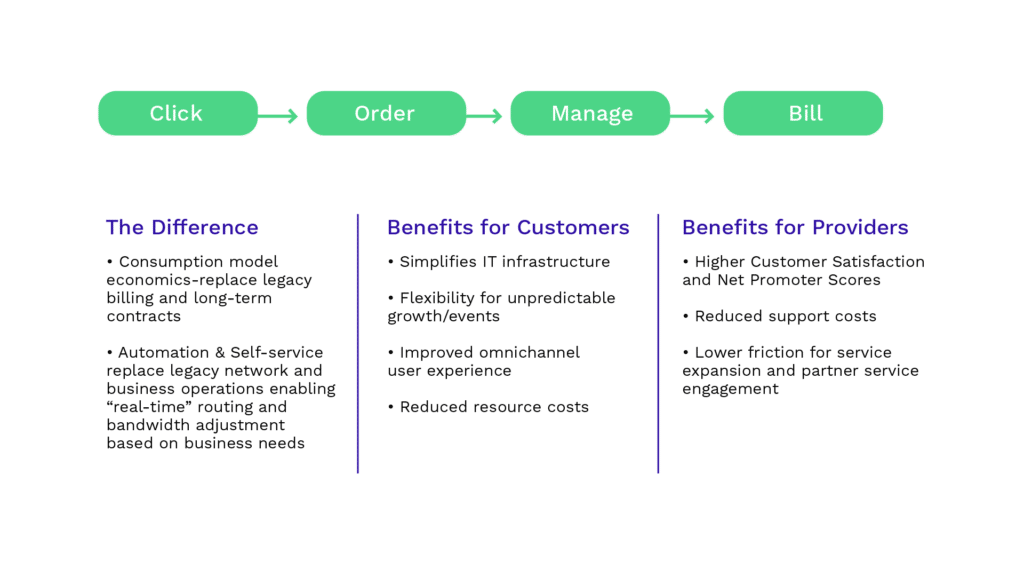

Cloud usage model meets the Business Internet

The new consumption model for Enterprise communications services is “Click, Order, Manage, Bill”.

Network-as-a-Service Model

Disruptive Billing is Key

Disruptive billing within our Converge platform facilitates the “Click, Order, Manage, Bill” consumption economic mode. Specifically, our platform enables flexible and dynamic pricing based on Geography, Metro/Long-Haul, Bandwidth/Capacity or Port Type. Customers select from options ranging from subscription-like format with 30-day payment terms up to multi-year contracts depending on connectivity needs, demands and strategy. PacketFabric takes away red tape and delays, using routine credit risk analysis to expedite our onboarding timeline without requiring collateral and automating the handling of any required paperwork.

The agility afforded by our ownership of our billing functionality has allowed us to add features in timeframes that defy the glacial and expensive telco/BSS-vendor dictated timeframes. In the last year, we have added:

- Hierarchical billing for resellers to be able to manage multiple levels of partners from MSP, to distributors, to VARs to end customers

- Burst billing appropriate for spot disruptions or cyclical operations

- Flex (Aggregate) billing to optimize terms for spending across the network

Not all XaaS is NaaS

XaaS models are popular with businesses because they simplify IT infrastructure and operations. Access and WAN are no exception, but hadn’t been available aaS. Unfortunately, with the rise and market acceptance of NaaS, everyone and every technology has tried to hitch their cart to the concept and it has caused some confusion.

Everyone knows what Network-as-a-Service (NaaS) is, but it seems no two definitions are the same. We want to clearly define true NaaS and in doing so show why using the right NaaS (a True NaaS) matters.

NaaS has 3 basic components;

- Pricing: Naas follows the cloud consumption model for software and hardware availability.

- Automation: At its most basic, its automated provisioning. But complete automation also exposes telemetry/monitoring and is what makes NaaS integrate-able; upward into the Service Layer, laterally through NNIs or directly as a parallel instance into another carrier operation or into Enterprise netops and devops processes. Automating requests for more or less bandwidth, change in path, new address ranges, real-time remediation.

- Self-service enablement: NaaS gives customers direct control over network bandwidth, reliability and connectivity needs and usage patterns in real-time and on-demand.

Confusion in “NaaS” categorization starts when an offer includes some, but not all of the basic components. For example, all claimants will point to the cloud consumption model as validation of NaaS inclusion. True NaaS has all of this base functionality as a starting point.

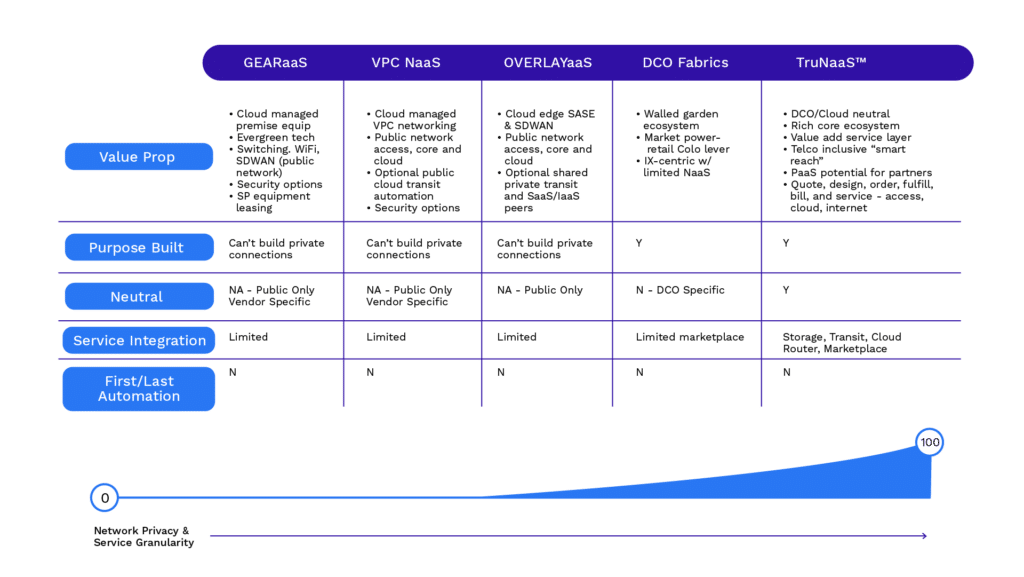

True NaaS goes further and is built upon a few additional exclusive and fundamental constructs:

Purpose Built Platform – True NaaS is a cloud native, API-first platform capable of scaling to meet the growth needs of customers. By design, a true NaaS builds private connections under the operator’s full control and adaptable to required technology – ultimately down to wave granularity. CI/CD feature and maintenance delivery combined with intelligent topology design provide private connections with strong SLAs.

Neutral market position – True NaaS is neutral across the spectrum of DCO, CSP, transit and fiber operators, without bias or lock-in. No requirements of special or proprietary equipment.

Service Integration support – Services built IN the true NaaS layer don’t require incremental per-customer equipment (NaaS is inherently multi-tenanted). Our own Virtual Cloud Router and integrated storage services are examples of integration IN NaaS.

An example of services built ON true NaaS would be SaaS applications like cloud-edge SASE. They are essentially API enabled:

- Physically through a NaaS Marketplace mechanism and/or

- Logically through an inter-platform API call

- Transparently like the intelligent NNI connectivity for telco partners

Extensible to the premise – True NaaS automation includes all the critical elements of: design, order, price, fulfillment, billing, and customer service. Complete control of access, cloud, and internet – end to end.

That is our vision at PacketFabric. With the addition of Unitas Global assets, the process of extending NaaS to your premise is here, and with it comes a new way of looking at not only how you connect but also how you consume the basic services to support a new business architecture. And, for all our customers, Unitas Global transit and peering become NaaS services – providing real business internet in addition to private site-to-site and cloud connectivity.

While last mile services ‘time to first deployment’ remains the long pole, NaaS innovates back office processes to make even these operations an on-line experience – all trackable, no calls needed. We automate everything, and it’s fully programmable – the value is future-proof.

We Are A Software Company: The White Label/Platform Opportunity

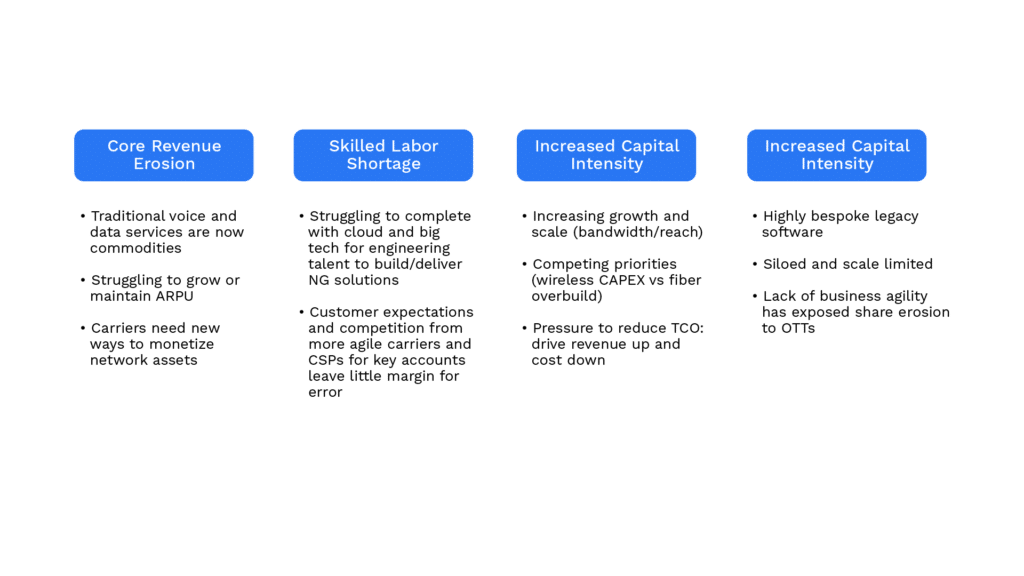

Traditional telcos face a number of well-known challenges: core revenue erosion, skilled labor shortages, increased capital intensity and outdated software systems.

Traditional telco may have fiber incumbency (also their achille’s heel) but no brand recognition in cloud services. And, NaaS transformation dreamed of by telcos is operationally impossible on existing brownfield deployments because of their decade-old, legacy SW stacks.

The requirements for telco to overcome these challenges and exploit their assets are:

- Corporate orientation toward a XaaS model

- Stack ownership (Best of Breed bespoke systems will fail to be agile)

- A completely new software implementation that is or mimics PacketFabric

Recent M&A activity validates that traditional telcos both see the opportunity and the challenge with KT acquiring Epsilon and PCCW Global acquiring Console Connect.

To compete as a cloud service provider, you need to own your stack and PacketFabric can provide an alternative – our stack as a new telco PaaS for wireline (fiber) telco. This positions PacketFabric into an even broader opportunity – the Telecom Software Solution market.

This market is described by Houlihan Lokey Commentary/Analysis:

- Highly recurring revenue with attractive unit economics / gross margins (80%+) for product driven businesses.

- High net retention driven by highly sticky products; almost entirely infeasible to rip and replace an in-place system; evidenced by operators continuing to work with vendors they’ve struggled with for decades.

- Software based solutions provide inherent operating leverage and ability to quickly achieve scale, customer base diversification and end market diversification.

- Significant barriers to entry; vendors benefit from being telecom-first and telecom focused when selling to CTOs, evidenced by horizontal software providers acquiring vertically-focused vendors.

Cloud Service Providers (CSPs) have the potential to be NaaS providers. They have the software capabilities telcos lack, and experience with XaaS infrastructure operation (IaaS, SaaS and PaaS) and economics. And while the larger CSPs provide transit across their backbones, it is costly and complex to orchestrate. A third-party market is as far as the CSPs have shown willingness to participate, which performs nothing like a commercial true NaaS service.

Enterprises are unlikely to adopt CSP backbones as they are today because they are unable to provide visibility, reported OAM and traffic and path inspection. Today, the lack of these features prevent any regulated industry from using CSP backbones, even between regions.

It’s unlikely for CSPs to provide a commercial NaaS platform like PacketFabric. To the CSPs, WAN is an opportunistic business. The use of a CSP backbone for global transit is an optimization of an existing expense in support of their REAL primary business functions. Any potential consumer has to realize that, when push comes to shove, THOSE businesses are preferred on their networks.

- They have no incentive to spend capital that could be spent to grow their primary businesses to connect beyond their own premises and solve business networking problems for telco or enterprise customers.

- They have no incentive to connect their customers to other cloud providers or DCO competitors.

- They have no incentive to take on the regulatory requirements.

To an even greater degree, their large DCO sistren are also unlikely to provide a global commercial NaaS solution. Besides having the same lack of incentive, they have arguably less software capability and have much more stringent capital restrictions (as they operate under REIT structures).

The incentives of these industry players is the antithesis of a vision to transform the internet for business. As Larry Ellison said recently when expounding on his “internet of clouds” concept:

“The original clouds were walled gardens. Moving data in seemed like a good idea, but then customers found that moving data out was a bad idea because of the fees associated with it. Those ingress and egress fees—that was the beginning of true multi-cloud.”

The existing vendors in the Telecom Software Solution Market, both equipment vendors and the old guard of telecom OSS/BSS providers, are providing DIY kits and NFV automation solutions that are already obsolete. And, the few cloud providers capable of providing a commercial NaaS platform have no incentives to do so.

In an XaaS market for WAN that is rapidly reaching an inflection point, the PacketFabric Converge platform is the key to unlocking traditional telco participation.

Our Business motion is one of Partnership as aVNO

Every network service provider (SP) needs to have a strategy for managing CAPEX while expanding service reach and capability – a smart growth strategy. PacketFabric has been establishing relationships with multiple telcos as part of such a strategy. We think this model solves shared investment (CAPEX) problems for both parties:

- Increases PacketFabric network reach while enabling SPs to focus CAPEX on growing connectivity in their core ecosystem – to DCOs, clouds and cloud services providers.

- Alleviates the need for SPs chase new on-ramp and data center installations out-of-their local geography for customer cloud needs

- Enables SPs to reach clouds and DCOs they don’t reach and provide a cloud service to their existing business customers, Adding net new revenue and saving cost.

Under the hood, PacketFabric is itself a VNO (Virtual Network Operator) and we can stitch multiple carriers at multiple technology layers.

Today, these relationships usually manifest as ENNI connectivity between our networks enabling Layer 2 and Layer 3 services. And, these partnerships are normally limited by the capabilities of our partners. The best integrations are via a combination of API mapping and Network-to-Network Interconnection (NNI) – assuming that the partner has an API-driven NaaS of their own.

One example of our many telco partnerships, has helped us expand our services in Europe, exposing 600+ DCOs in the partner geography to our customer base with a fully integrated look and feel. The partner customer has fully-automated reach to PacketFabric’s fabric and PacketFabric customers have automated access to partner’s DCs directly through the UX and APIs.

For a number of reasons, traditional telcos have been slow to convert to an API driven NaaS operation, which opens a Platform-as-a-Service partner opportunity to PacketFabric.

NaaS fabrics have to figure out physical, logical and BUSINESS levels of “peering” to provide end-to-end NaaS services. The alternative is no seamless global coverage or global-but-single-vendor provided by a big well-capitalized cloud provider – a walled garden that nobody really wants.

Like the ubiquitous S3 API for object storage today, a good production-tested connectivity API set that works between Network as a Service (NaaS) providers without a translator would ultimately be a positive step. But that step will never be taken. There are issues around the sharing of service and inventory catalogs at a useful granularity, starting with the telco addiction to legacy systems safeguarding that information. And creating a standard in the telco world for a rapidly evolving opportunity is a foolish goal. Between the IETF, TMForum, MEF, ETSI and ITU you’re likely to get more than one definition after a decade of work. Most of these organizations are not even focusing on the target. There are a few low-level provisioning APIs that have been around for years that are the only thing available. Efforts in OpenSource have turned into folly and are wholly missing the mark of where the trajectory the industry is on. Right now, the one that makes sense is Terraform; and we’ve gone big.

The white labeling of PacketFabric by traditional telco obviates this need. PacketFabric has defined the industry standard by delivering it. A huge opportunity has opened for the PacketFabric Converge platform to run their assets.

WAN or cloud-core network partnerships aren’t the only fit for the PacketFabric Converge platform in Telco. Our abilities run from edge to cloud, so we can run and optimize the operation of any subset of the Telco network in-between: full metro networks, metro to in-building and regional aggregation networks. In many cases, capital expenditures to upgrade these subsets to fiber will require a new software approach to optimize revenue generation.

And Telcos aren’t the only provider partner opportunity for the PacketFabric Converge platform. Only a few of the numerous DCOs worldwide have approached the level of NaaS automation for their own site-to-site connectivity, which is essential to their customer base. The impediments are not only the technical hurdle of developing a platform, investing the capital to build their interconnecting fabric.

As mentioned earlier, the few who have invested lack incentive to provide further connectivity outside of their premises. None integrate well with NaaS fabrics to seamlessly broaden their market and rely instead on telecoms meet-me rooms and the arcana of the past generation of network connectivity.

For those other DCOs, connecting to our fabric (if they lack the capital and expertise to operate their own WAN) and/or white labeling PacketFabric Converge platform to run their assets is yet another large opportunity.

III. Nothing Less Than Revolutionizing the Internet Architecture

In summary, our goal is nothing short of transforming the Internet from the stranglehold of telcos, CSPs and those that want to create walls of connectivity and business.

We remain fiercely agnostic in our partnership model.

- We will work with telcos as fiber and access companies, yet put our value added true NaaS platforms on top of them.

- We will work with CSPs, yet optimize connectivity with a fabric architecture for data-in-motion between them and enable enterprises to select the right CSP for the job and price.

- We have a proven model: PacketFabric has successfully partnered with several DCOs who want to offer network service to compete with the behemoths that want to limit the utility of all the private data-center space available.

The goal is to be THE full Edge-to-Everywhere NaaS platform that powers all these service alternatives.

The key to the realization of our future is as a software company. We have delivered both our vision and the ability of our platform by running and operating our own network. We are literally eating our own dogfood. We’ve grown revenue and adoption ahead of our own projections, and filled a massive hole in the internet architecture.

In the process we’ve rejected the traditional OSS/BSS industry that was built on the call data record, we’ve rejected the notion that the only Service Providers are ones that own fiber or data center operators or are CSPs. PacketFabric fully pushes fiber owners to commodities and builds the internet from the best supplier, at the best cost with agnosticism.

PacketFabric’s future as a software company is one based on the scale-out capability of a cloud native platform on top of a distributed system.

- We can run other companies’ networks as we operate our own.

- We can operate all aspects of connectivity service delivery

- We can not only instantiate other instances of our platform for others, but manage and operate the platform CI/CD.

Shrink-wrapped software running “on-prem” is the antithesis of being agile and “continuous.” This is where PacketFabric excels. It’s hard to imagine a better way for traditional telcos to bring NaaS operation to their facilities than having PacketFabric technology manage and operate their network.

It’s even harder to imagine why an enterprise would own-manage and operate their own network any longer or suffer the stagnation of telco-cement or hoping that the internet swamp will deliver my packets bound in an overlay. A true NaaS and fully programmable private Internet is here to replace decades of the legacy IT software stack and decades of bandaids. Low friction, easy to use by non-networking-specialized labor, PacketFabric enables enterprises to focus solely on their business and not the “context.”

The future of the internet isn’t in the three planes of forwarding, control and management planes; those are constructs thrust upon us by system integrators and industry luminaries. We are focusing on building the best fully programmable internet with a Network as a Service platform.

Enterprise and telco networks aren’t currently built for real-time, programmatic control. And, decentralized data, IT and apps and data and security that run out of multiple cloud services, and a distributed, mobile workforce break traditional networking.

While a dizzying array of technologies and hundreds of vendors in a highly fragmented marketplace are trying to solve parts of this problem, PacketFabric fully simplifies the problem.

We provide connectivity without friction through our platform IP:

- SaaS applied to Networking = NaaS

- In building (edge) to everywhere (full fabric) in real-time

- Provision, monitor, manage, account via APIs and UX

- Design, Quote and Deploy in seconds

- Fully integrated with networking and service partners

It is the most mature, feature rich NaaS platform in the industry that fully transforms enterprise networking by changing the way we deliver the internet.

Our message to Enterprise CTOs and CIOs is “Reimagine your ENTIRE business operation. PacketFabric enables an Enterprise to design and control their communication architecture; while not having to carry the burden of owning and operating any part of their network.”

Our message to telcos and DCOs is “why just talk about strategic plans for adopting NaaS, partner with PacketFabric and be in business today.”